.jpg)

25 March, 2020

The National Assembly adopted the new Law on Securities (the "New Law") with a view to improving the current legal framework of the securities market by further aligning it with the overall development scheme of Vietnam's financial sector. The New Law will replace the current Law on Securities (together with its implementing regulations, the "Current Law") with effect from 1 January 2021.

We have highlighted some of the New Law's key changes and provisions below.

1. Foreign ownership limitations in public companies

Under the Current Law, if a public company conducts business within certain business lines that are subject to conditions imposed on foreign investors, and if there are no specific provisions on the foreign ownership limitation (the "Undetermined Conditional Sectors"), the foreign ownership ratio is capped at 49% of the voting capital. If a public company wishes to lift its foreign ownership ratio to above 49%, it has to prove that none of its business lines fall within the Undetermined Conditional Sectors, which may not always be a straightforward process.

Once in effect, the New Law will specifically delegate such matters to the Government. In particular, the Government will be responsible for issuing detailed regulations on foreign ownership limitations and conditions as well as procedures for investment and participation in the securities market by foreign investors and organizations with foreign capital.1 This provision is aimed at providing leeway for the Government to regulate foreign ownership in conditional business sectors in alignment with proposed amendments to the Law on Investment.

2. New conditions for public company status

Under the Current Law, a joint stock company has to register its public company status with the State Securities Commission (the "SSC") if it falls under one of the following categories:

(a) it has conducted a public offering;

(b) it has shares listed on a stock exchange or a securities trading center; or

(c) it has 100 shareholders, excluding professional securities investors ("PSIs"),2 and a charter capital of VND 10 billion3 or more.

Under the New Law, a joint stock company will be considered a public company if it falls into one of the following cases:

(a) Case 1: It has a paid-up charter capital of VND 30 billion4 or more (as compared to VND 10 billion5 under the Current Law), and has at least 10% of its voting shares owned by 100 or more investors who are not major shareholders;6 or

(b) Case 2: It has successfully conducted an initial public offering ("IPO").7

Under the New Law, a private company that becomes a public company because it meets the criteria on capital size and shareholding structure in Case 1, must:

(a) apply for registration of its public company status with the SSC within 90 days from the date it meets the conditions in Case 1;8 and

(b) place its shares for trading on the unlisted securities trading system (Unlisted Public Company Market – UPCoM) within 30 days of confirmation by the SSC of the registration of its public company status. Such company may apply for listing two years after the date that its shares are first traded on UPCoM.9

The New Law entitles the SSC to consider cancelling the public company status of any company that, for a period of one year or more, fails to (i) maintain its charter capital at the minimum of VND 30 billion,10 or (ii) have at least 10% of its voting shares owned by 100 or more investors who are not major shareholders.11

As part of the transitional provisions, companies which have their shares listed or traded on UPCoM before 1 January 2021 will not be forced to deregister their public company status if they fail to meet either of the above two conditions, unless otherwise decided by their general meeting of shareholders.12 If an existing public company, which has not had its shares listed or traded on UPCoM before 1 January 2021, fails to meet one of the above two conditions, it will have its public company status cancelled.13

3. New conditions for public offerings

The New Law sets out different conditions for an initial public offering ("IPO") and a subsequent public offering.

Under the New Law, an IPO is subject to the following conditions, inter alia:14

(a) the company has a paid-up charter capital of at least VND 30 billion15 (as

compared to VND 10 billion16 under the Current Law);

(b) the company must be profitable for two consecutive years preceding the year of the IPO (as compared to one year under the Current Law);

(c) at least 15%, or 10% in case the company has a charter capital of VND 1,000 billion17 or more, of the company’s voting shares must be sold to 100 or more investors who would not become major shareholders following the IPO. If this condition is not satisfied, then the IPO will be cancelled18 and the company will be required to refund all payments to the respective investors within 15 days of the cancellation;19

(d) shareholders classified as major shareholders of the company before the IPO, must undertake to collectively hold at least 20% of the company’s charter capital for at least one year after the completion of the IPO;

(e) the shares of the company must be listed or placed for trading on UPCoM following the end of the IPO; and

(f) the company is not criminally prosecuted and does not have an un- expunged criminal record on violations of economic management orders.

The New Law requires that any company accomplishing an IPO must have its shares listed or placed for trading on UPCoM within 30 days of the completion of the IPO, reduced from one year under the Current Law.20

Under the New Law, the conditions for a public company to conduct a subsequent public offering include, inter alia:21

(a) the company has at least VND 30 billion22 of paid-up charter capital (as compared to VND 10 billion23 under the Current Law);

(b) the total par value of the offered shares must not be greater than the total par value of the outstanding shares in circulation, unless the company issues shares (i) using the owner's capital, (ii) for the conversion, consolidation or merger of companies, or (iii) has an underwriter that

undertakes to purchase all shares of the company for resale, or purchase the shares of the company that have not been allotted;

(c) if the offering is to raise capital for a project of the public company, at least 70% of the total offered shares must be sold. If this condition is not satisfied, then the subsequent public offering will be cancelled24 and the company will be required to refund all payments to the respective investors within 15 days of the cancellation;

(d) the shares of the company must be listed or placed for trading on UPCoM following the end of the subsequent public offering; and

(e) the company is not being criminally prosecuted and does not have an un- expunged criminal record on violations of economic management orders.25

4. New conditions for private placements

Under the Current Law, a "private placement of securities" is an offering of securities to less than 100 investors, not including PSIs, and without using mass media or the internet.

The New Law redefines "private placement of securities" as an offering not conducted via mass media to (i) less than 100 investors, exclusive of PSIs, or (ii) to PSIs only.26 Further, the New Law expands the definition of PSIs to include:

(a) commercial banks, branches of foreign banks, finance companies, insurance trading organizations, securities companies, securities investment fund management companies, securities investment companies, securities investment funds, international financial organizations, off-budget State finance funds and State finance funds authorized to acquire securities;

(b) companies with paid-up charter capital of above VND 100 billion27 or companies whose shares are listed or registered for trading on UPCoM;

(c) individuals holding securities practicing licenses;

(d) individuals holding portfolios of securities listed or placed for trading on UPCoM with a value of at least VND 2 billion28; and

(e) individuals with a taxable income of at least VND 1 billion29 in the most recent year.30

The New Law specifies that for the private placement of shares by a public company, the shares can only be offered to strategic investors31 and PSIs.32

Under the Current Law, all shares issued through a private placement by a public company are subject to a one-year lockup (subject to certain exceptions), regardless of the type of subscriber. This is amended under the New Law so that the transfer restriction period will be at least three years for strategic investors and at least one year for PSIs (except in certain stipulated cases).33

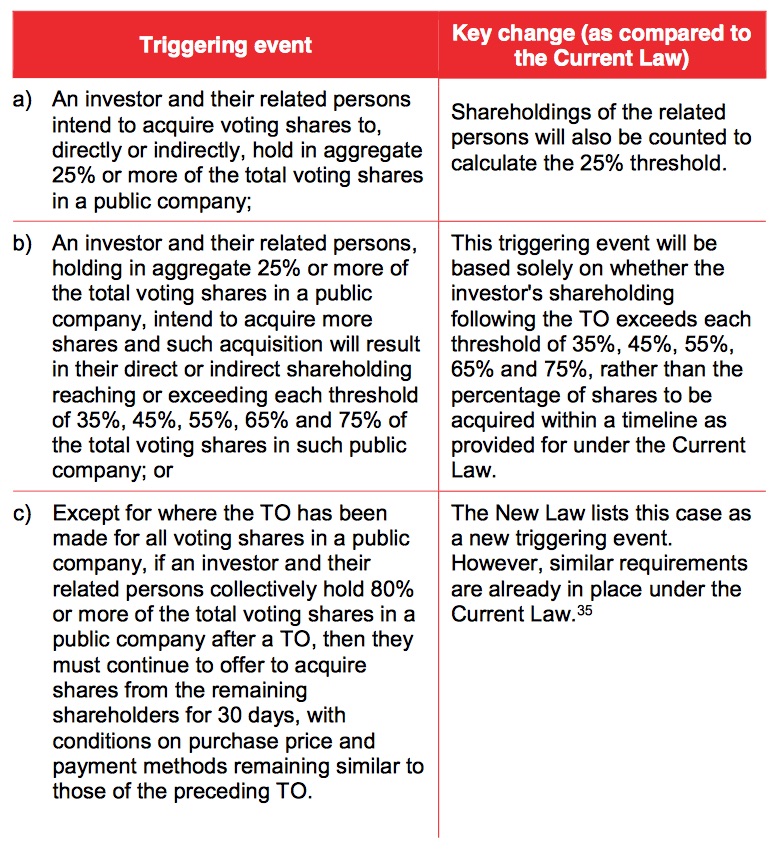

5. New triggering events of tender offers

The New Law provides for new circumstances in which a proposed purchase will trigger a tender offer ("TO") by a purchaser:34

The New Law counts indirect shareholdings in calculating the acquisition threshold to decide whether a TO is required, however it does not clarify how "indirect" shareholding is to be defined.

Under the New Law, a TO is not required for the acquisition of State capital or capital owned by State-owned enterprises in another enterprise.36

6. New conditions for public companies to redeem shares

Under the Current Law, a public company is entitled to redeem shares (subject to certain conditions) and retain them as treasury shares, the total par value of which constitutes part of the charter capital.

In line with the Law on Enterprises, the New Law will require public companies to reduce their charter capital by an amount equal to the total par value of any redeemed shares. Such a reduction must be made within 10 days of full payment for the redeemed shares, or, with respect to ESOP shares, within 10 days of reporting the total ESOP shares redeemed from employees to the annual general meeting of shareholders.37 However, the New Law allows a public company to immediately sell the redeemed shares where (i) it redeems shares to correct transaction errors or to redeem odd-lot shares,38 (ii) it redeems shares in accordance with a plan to issue shares for paying dividends or a plan to issue shares using the owner's capital, or (iii) it redeems odd-lot shares at the request of shareholders.39

7. Expanded definition of "related persons"

The New Law provides for a broader definition of "related persons" as compared to the Current Law.40 For example, under the New Law, related persons of a public company also includes the company secretary, the person in charge of corporate governance and anyone authorized to disclose information of the company. All persons defined as "related persons" under the Law on Enterprises will also be regarded as "related persons" under the New Law. This expanded definition broadens the applicability of the provisions of the New Law which refer to related persons, including provisions on TO triggering events and obligations to prevent conflicts of interest and disclose information.

8. License of securities companies and fund management companies

Under the Current Law, the establishment and operation license of securities companies and fund management companies issued by the SSC can also serve as their enterprise registration certificate.

Under the New Law, this provision will no longer apply. Instead, a securities company or fund management company will have to first obtain an establishment and operation license from the SSC, before also obtaining an enterprise registration certificate from the local Department of Planning and Investment, as per the Law on Enterprises.41

The New Law also introduces minor changes to the conditions for the establishment of new securities companies and fund management companies. Securities companies and fund management companies established before the New Law takes effect will also have to satisfy these conditions and obtain an enterprise registration certificate within two years from the effective date of the New Law.42

For further information, please contact:

Yee Chung Seck, Managing Lawyer, BMVN International LLC,

member of Baker McKenzie International

tmh@bmvn.com.vn

1 Article 51, New Law.

2 The Current Law defines "professional securities investors" as commercial banks, finance companies, finance leasing companies, insurance trading organizations and securities trading organizations.

3 Approximately US$ 431,000.

4 Approximately US$ 1,293,000.

5 Approximately US$ 431,000.

6 Under the New Law, major shareholders are defined as shareholders who each own 5% or more of the total voting shares.

7 Article 32.1, New Law.

8 Article 32.2, New Law.

9 Article 34.1(d), New Law.

10 Approximately US$ 1,293,000.

11 Article 38.2, New Law.

12 Article 135.4, New Law.

13 Article 135.5, New Law.

15 Approximately US$ 1,293,000.

16 Approximately US$ 431,000.

17 Approximately US$ 43,100,000. 18 Article 28.1(b), New Law.

19 Article 28.3, New Law.

20 Article 29.2, New Law.

21 Articles 15.2 and 26.4, New Law. 22 Approximately US$ 1,293,000.

23 Approximately US$ 431,000.

24 Article 28.1(c), New Law.

25 Article 28.3, New Law.

26 Article 4.20, New Law.

27 Approximately US$ 4,310,000. 28 Approximately US$ 86,200.

29 Approximately US$ 43,100. 30 Article 11, New Law.

31 Under the New Law, strategic investors of a public company are investors selected by its general meeting of shareholders, based on their financial capacity and technological expertise, who undertake to cooperate with the company for a period of at least three years.

32 Article 31.1(b), New Law.

33 Article 31.1(c), New Law.

34 Article 35.1, New Law.

35 Article 51, Decree No. 58/2012/ND-CP (as amended).

36 Article 35.2(d), New Law.

37 Articles 36.5 and 36.6(b), New Law.

38 Odd-lot shares refers to a number of shares that are not sufficient to form a lot of shares to be traded on the relevant stock exchange.

39 Article 36.7, New Law.

40 Article 4.46, New Law.

41 Article 71.1, New Law.

42 Article 135.2, New Law.