21 March, 2020

Below is an overview of the reporting standards for financial account information in Thailand following the enactment of the Amendment of the Revenue Code Act (No. 48), B.E. 2562 (the "Amendment of the Revenue Code Act") and Ministerial Regulation (No. 355) re: Reporting Obligations of a Person with Special Transactions, which require reporting financial institutions to submit reportable financial account information to the Revenue Department by 31 March of every subsequent year.

-

Who is obliged to report?

-

Financial institutions including commercial banks, specialized financial institutions, finance companies, and credit foncier companies.

-

E-payment service providers.

-

-

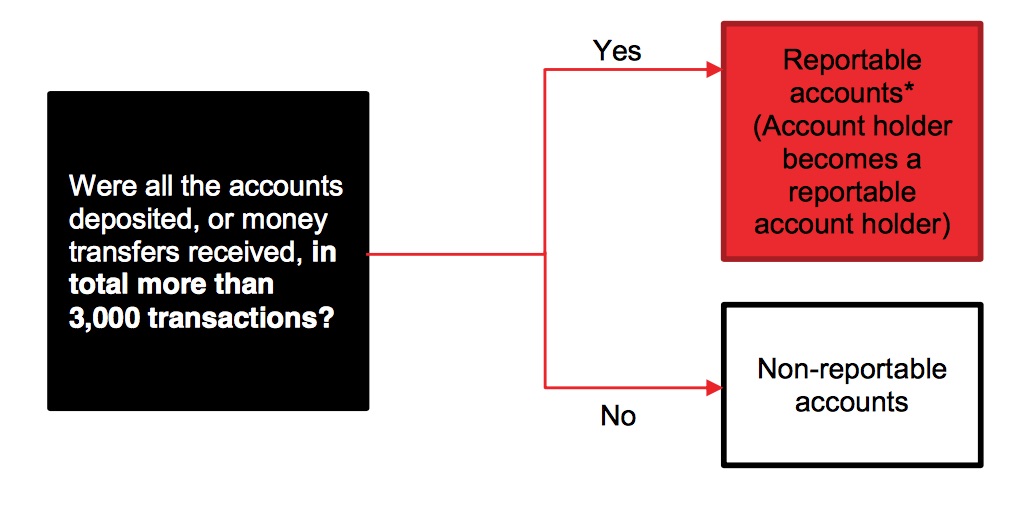

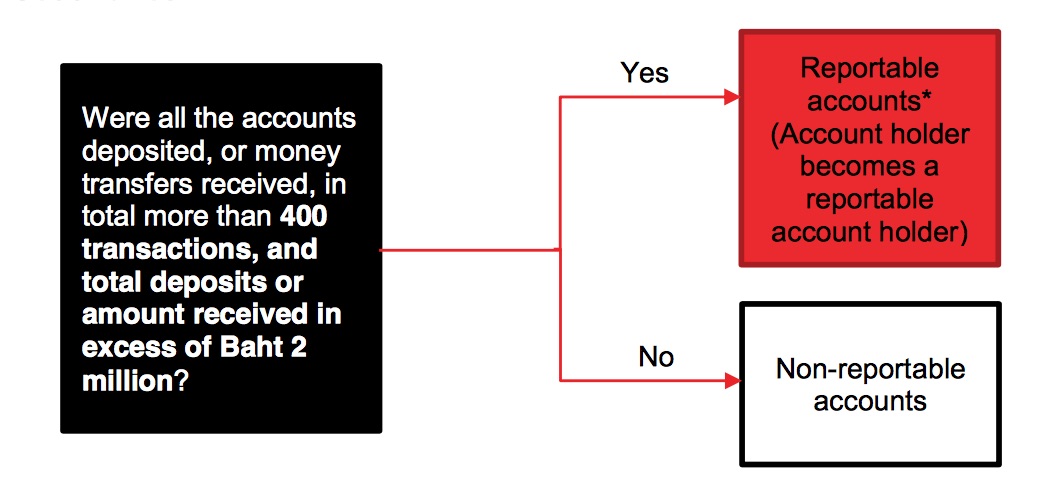

Reportable or non-reportable accounts?

Reportable accounts are accounts that have "special transactions" for the reportable calendar year. There are two tests to determine reportable accounts:

First test

Second Test

Remark* –

If an account held by an account holder is a reportable account, then all accounts held by that account holder at a specific reporting financial institution are regarded as reportable accounts.

-

What financial account information do reporting financial institutions need to report?

-

National ID number, passport number, corporate registration number, tax identification number, or other information to identify a reportable account holder.

-

Name and last name of a reportable individual account holder; name of a reportable unregistered partnership account holder; name of a reportable group of persons that is not a juristic person account holder; or reportable juristic person account holder name.

-

Total number of deposits or money transfers received for all reportable accounts.

-

Total amount of deposits and money transfers received for all reportable accounts.

-

All reportable account numbers.

-

-

Calculation rules for transaction quantity and value

-

Transaction quantity and value for every deposit and money transfer received must be recorded, regardless of the reporting financial institution's deposit policy.

-

Transaction quantity and value for every deposit and money transfer received via QR code or other e-payment channel must be recorded, regardless of the reporting financial institution's deposit policy.

-

Deposit or money transfer received in foreign currency must be calculated into Thai baht by using the Bank of Thailand's average buying rate as of the last date of the reporting year.

5. Effects on reporting financial institutions

Reporting financial institutions must submit reportable financial account information for the reporting year, to the Revenue Department, no later than 31 March of the subsequent year.

Non-compliance carries penalties of a fine not exceeding Baht 100,000 and a fine of Baht 10,000 per day until the reporting financial institution submits the reportable financial account information to the Revenue Department.

6. Effects on reportable account holders

-

Reportable account holders could be subject to tax audit, potentially resulting in tax assessment, if the Revenue Department finds incorrect tax payments.

-

Reportable account holders that do not file tax returns or incorrectly declare income to the Revenue Department could be subject to surcharge and penalties according to the Revenue Code.

The enacted bill will have detrimental effects on freelancers, illicit businesses, and, most importantly, on social commerce businesses (online shopping businesses on social media platforms). The bill is expected to help identify tax audit opportunities for the Revenue Department. The enacted bill may encourage individual taxpayers to use cash payments to avoid being reported, and may not be in line with the current government's Thailand 4.0 policy, which also aims to transform traditional money transactions into digitalized cashless transactions.

For further information, please contact:

Aek Tantisattamo Partner, Baker McKenzie

aek.tantisattamo@bakermckenzie.com